To ensure the strength of the derivatives market, SEBI announced changes earlier this week to maintain and improve market stability. Some of these changes may seem complicated for traders so we wanted to introduce you to them as well as provide an explanation. Many of these changes impact all futures and options traders but others only impact select traders that trade in certain strategies. Also, not all of these changes will be effective all at once. This is how these changes will affect your trading activities:

1) Upfront premium collection (Effective: February 1, 2025)

- What’s changing? Buyers will need to pay the full premium for options upfront.

- Why? This is to curb excessive speculation among retail investors.

- Example: Previously, you might have taken the position in option premium of ₹20,000 against stock or cash margin and would have actually paid ₹20,000 on settlement day, but from February 2025, you’ll need to pay the entire ₹20,000 at once and that too upfront, reducing the chance of over-leveraging.

2) Removal of calendar spread treatment on expiry day (Effective: February 1, 2025)

- What’s changing? A calendar spread strategy means entering into a contract of Near and Far months. Typically, a calendar spread strategy is selling an option contract with a near-term expiry and purchasing an option contract with a longer-term expiry. The longer-term option contract partially hedges the risks associated with selling the near-term option contract. Because of this, margin benefits have been applied to the short side of this contract. This change means that on expiry day, the margin benefits will no longer be applicable to the expiring near-term (short) option and traders will need to maintain a higher margin balance.

- Example: Assume you are trading a call calendar spread and are short the 31 Oct 24 expiry and are long the 28 Nov 24 expiry. When you entered into the trade, you would be provided margin benefit for the short call that expires on 31 Oct 24. As of now, this margin benefit continues through the expiry on 31st Oct 24. After this is effective, assume you enter into a similar call calendar spread with a short call option expiring 27 Feb 25 and long call option expiring on 27 Mar 25. You will still receive a margin benefit for the short call option when you enter into the strategy. However, this margin benefit will no longer be available after 26 February as you go into expiry on 27 February. This means to maintain the position, you need to post an additional margin on 26th Feb EOD as compared to 31st October 24 EOD, in our previous example.

3) Intraday position monitoring (Effective: April 1, 2025)

- What’s changing? SEBI will monitor intraday positions more closely, taking at least four random snapshots throughout the trading day.

- Why? Currently, SEBI monitors intraday positions on an end-of-the-day basis to ensure that a client hasn’t taken a position beyond permissible limits (5% at the client level & 15% at the broker level). Since it is possible for traders to take positions beyond permissible limits intraday and simply reduce them before the end of the day, SEBI will start monitoring more frequently. Specifically, beginning April 1, 2025, it will monitor on a real-time basis by taking at least four random snapshots, to identify if any client is exceeding the intraday limit set by SEBI. The measures are equivalent to monitoring of margin requirements by SEBI, through peak marking snapshots. This is to prevent excessive risk and market manipulation.

4) Increased contract size (Effective November 20, 2024)

- What’s changing? The minimum contract value for index derivatives will be increased to ₹15 lakh. The lot sizes will be revised so that the contract value stays between ₹15 lakh and ₹20 lakh during reviews.

- Example: Say currently, an option contract is trading at ₹400. This particular underlying security has a minimum lot size of 25 lots. This makes the total current cost ₹10,000 (₹400 × 25 = ₹10,000). However, after the SEBI changes, the future minimum lot size could increase to 75 lots. With the option price remaining at ₹400, the cost would instead be ₹30,000 (₹400 × 75 = ₹30,000). It’s a significant increase in total costs from ₹10,000 currently to ₹30,000 in the future, due to the increased lot size, despite the option price remaining the same.

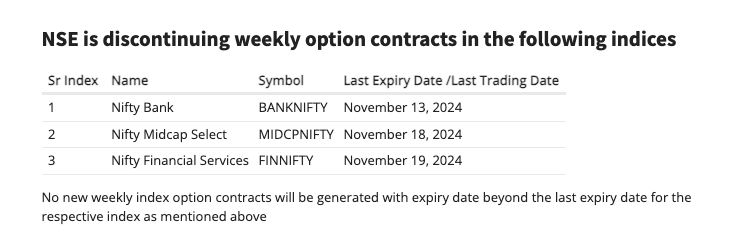

5) Rationalization of weekly expiries (Effective: November 20, 2024)

- What’s Changing? Only one benchmark index (like Nifty or Sensex) will have weekly expiries per exchange.

- Why? Expiration days are the most volatile for an option contract and are the most challenging days to navigate for a trader. This volatility, along with low premiums as a result of low time value remaining on the contracts, has led to speculative trading on expiries. This change will limit the number of trading opportunities on expiry days thus reducing speculative trading.

6) Additional margin for expiring contracts (Effective: November 20, 2024)

- What’s Changing? Extreme loss margin, or ELM, is an additional margin charged to minimize risk associated with market volatility. On expiry day, short contracts will require an additional 2% extreme loss margin. This is applicable to short trades that are entered into on expiry day as well as positions that are carried over to expiry from prior trading days.

- Example: Assume that you sell an option on Monday that expires on Thursday and it requires you to provide an ELM of ₹10,000. If you still hold this short position on expiry day, you will need to provide an extra 2%, or ₹200, in extreme loss margin.

These changes aim to create a more stable trading environment by reducing excessive speculation and increasing margin requirements. For F&O traders, this means adapting to stricter rules and potentially higher costs, especially regarding contract sizes and upfront premium payments.